Records tumble in AuctionsPlus sheep and lamb sales

There's no secret the sheep and lamb markets are firing, but it's record prices achieved on AuctionsPlus in recent weeks that have got tongues...

Recent rain which has sent young cattle markets into overdrive have overshadowed some of the developing headwinds, especially for finished cattle. The latest beef export data released last week shows the impact of Chinese beef tariffs, with reports out of the US of export pricing easing.

Finished cattle supply remained relatively strong in June, with cattle slaughter similar to last year, but off the peaks of May. Weaker slaughter saw less beef available for exports, with total beef exports down 4% on May, but interestingly it was still up 9% on June 2025.

With similar slaughter there was either a stronger proportion of beef exported, or higher slaughter weights. It was probably both, but we’ll have to wait for ABS quarterly slaughter and beef production data for confirmation.

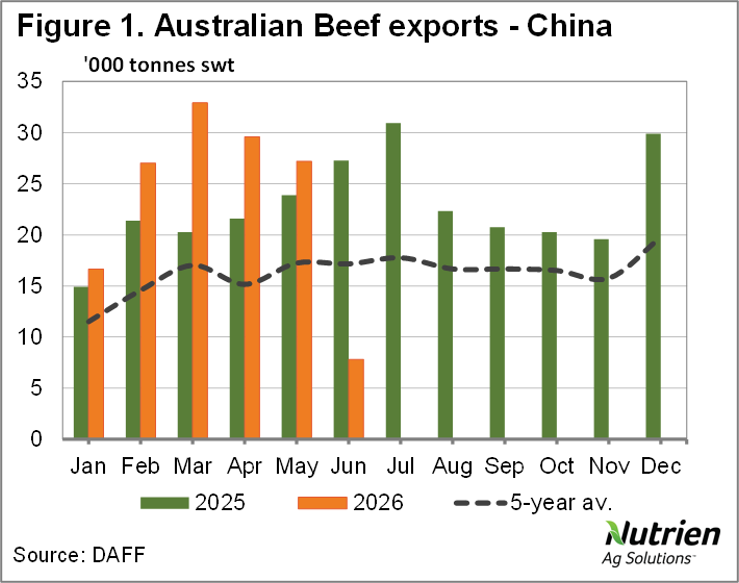

The big move was seen in exports to China, with the quota being met, and beef exports falling dramatically. Figure 1 shows beef exports to China fell 71% on both May and June last year, with monthly exports the lowest since 2016.

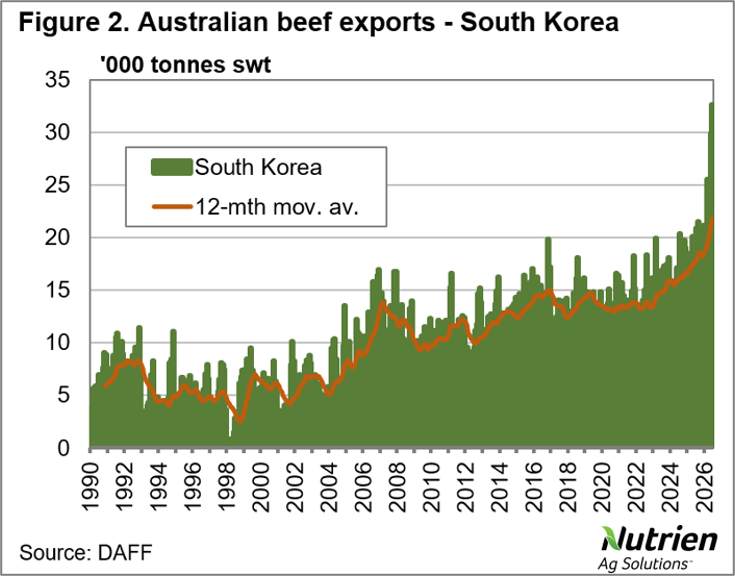

With Chinese volume available for other markets, it was spread around. Beef exports to South Korea were up 9% to their highest level since on record (figure 2) as processors rush to get beef in before that quota is filled.

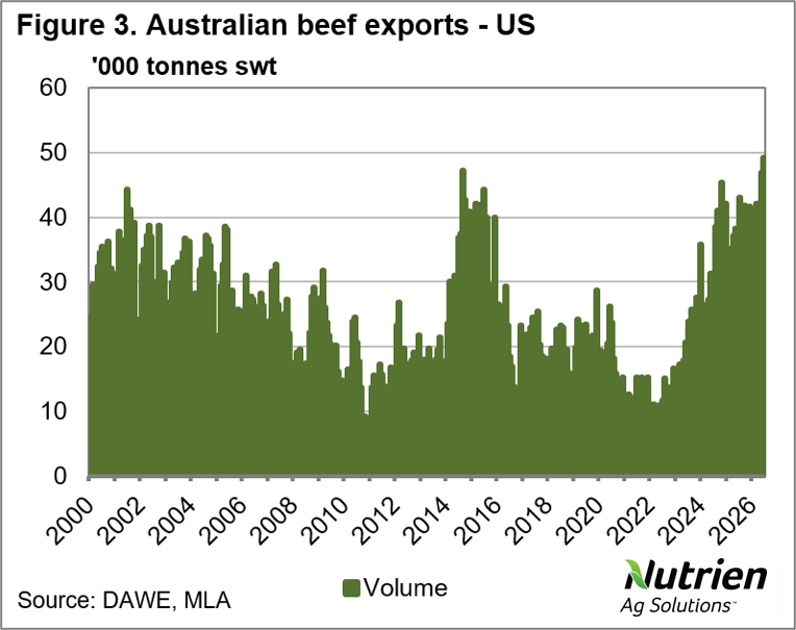

Our biggest beef export market, the US, also took more beef in June, with exports up 5% and also hitting a new monthly record (figure 3). Almost every other beef export market also received more beef in June, as exporters spread what was China’s share around.

Shifting product away from China seems to have come at a cost, with prices 90CL frozen cow prices easing through much of May and June. With more beef available for the US market, and seasonal weakening of demand in the US, it’s not surprising to see 90CL values fall. What is a little surprising is that they are still over 10% stronger than last year in US terms.

With the quota to South Korea close to being filled, tariffs will increase from 5.3% to 24% making our beef more expensive. The quota was hit last year in September, and export volumes were minimally affected for October to December, however exports were much lower last June compared to this year.

What does this mean?

June export data has shown how beef exporters can pivot, with work to expand markets over the past 20 years paying off. There will be impacts on export prices however, and this can impact finished cattle prices, which have remained steady in the face of rising young cattle values.

It is hard to see much upside in finished cattle prices while exports are restricted, and it’s hard to say what will happen in January, with weather having a big say between now and then.

Beef exports to China fell heavily in June as the quota was filled.

Other markets took more beef, with Korea and the US both seeing new record volumes.

Angus Brown brings over 20 years of expertise analysing Australian agricultural markets, and also runs a mixed farming operation in Hamilton, Victoria.

Angus Brown brings over 20 years of expertise analysing Australian agricultural markets, and also runs a mixed farming operation in Hamilton, Victoria.

There's no secret the sheep and lamb markets are firing, but it's record prices achieved on AuctionsPlus in recent weeks that have got tongues...

The global beef market discussion was focussed primarily on the United States for much of the past few years - until China made headlines with new...

The set up is complete - now all signs point towards a central eastern Australia rebuild shaping the market come Spring 2026.