Weaner steer premium lifts to 20% amid increased northern supply

The Weaner Steer Premium lifted to 20% last week as the market adjusted to increased turnoff, largely driven by seasonal conditions across northern...

In the midst of a conflict driven fuel crisis, and the wide-ranging impacts on the supply chain and logistics the cattle market has remained relatively stoic. If anything, young cattle prices have rallied, with rainfall seemingly trumping uncertainty.

The widespread rainfall and flooding through northern and central Australia, along with the Riverina has seen some of the premium return to the weaner cattle market in southern Australia.

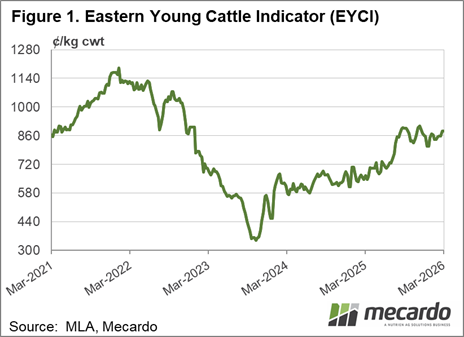

The Eastern Young Cattle Indicator (EYCI), which, at this time of year, and for most of the time if we think about it, is dominated by northern markets, has rallied nearly 5% since the end of February. As of Tuesday the EYCI is at close to 900¢/kg cwt (figure 1), which at 54% comes in at 486¢/kg lwt.

A quick scroll through AuctionsPlus shows Angus Steers from 250-300kgs in southern NSW are selling in a broad range but averaging around 550¢/kg lwt. Historically this is a pretty good premium to the EYCI. Moving further south, price creep higher, with some lighter steers selling over 600¢/kg lwt.

We had a query on the cost of freight, and what rising diesel prices might do to geographic price spreads. Without being an export on truck fuel consumption, a few sources on the internet tell us B doubles will use around 42 litres of diesel per 100km. With diesel prices rising from $1.80 per litre to $2.60 and higher in regional areas, this adds $32 per 100km.

If you can get 108 weaner steers at 300kg on a b-double the extra cost comes in around 30¢/head per 100kg. If steers are transported 500kg the increased cost of diesel is 0.5¢/kg lwt. It seems very low but the extra cost for a 500km haul is $160, divided by 32,400kgs.

The increased freight costs are unlikely impacting geographical spreads, apart from maybe perceived extra costs. The higher prices in the south are more likely due to destocking over the past two years, and a drive to get more mouths.

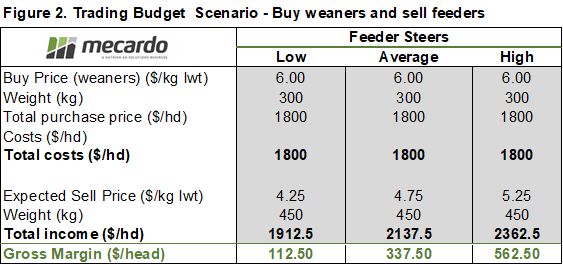

Figure 2 shows the potential margins on buying 300kg weaner steers for 600¢ and growing out to export feeders. Margins look ok, historically, if feeder prices can hold at the levels we have seen since September last year. If feeder prices fall back towards the 400¢ level, the trade will have all been for nothing.

Note that this trade calculation does not include feed, freight, treatments, or administrative costs. These will differ between enterprises and should be assessed individually when considering any trade.

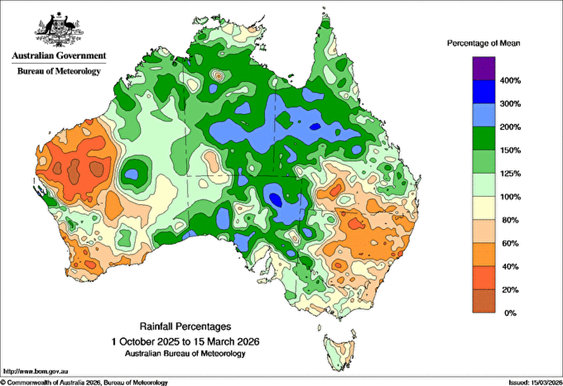

It is interesting to see light cattle making such a premium over feeders and the EYCI given the current market uncertainty. Key cattle and cropping areas in Northern NSW have had a dry summer (figure 3), with the Bureau of Meteorology forecasting a strong probability of a drier than normal autumn and early winter.

On the upside global beef prices remain at extreme levels, and any tightening of supply due to season or otherwise here will be met with higher prices.

Angus Brown brings over 20 years of expertise analysing Australian agricultural markets, and also runs a mixed farming operation in Hamilton, Victoria.

Angus Brown brings over 20 years of expertise analysing Australian agricultural markets, and also runs a mixed farming operation in Hamilton, Victoria.

The Weaner Steer Premium lifted to 20% last week as the market adjusted to increased turnoff, largely driven by seasonal conditions across northern...

.png)

Ripley Atkinson assesses the major upside and downside factors shaping the outlook for Australia’s beef sector.

The conflict in the Middle East has had minimal impact on local grain or livestock prices as of yet, especially sheep meat. Forward pricing for lambs...