Matt Dalgleish

Matt Dalgleish

Sheep clearance hits seven-year high as AuctionsPlus livestock trade strengthens in FY26

AuctionsPlus has recorded its strongest sheep clearance rate in seven years, with FY26 figures showing renewed confidence in the online livestock...

The US cattle market entered 2026 appearing to sit right on the edge of a meaningful herd rebuild. Female slaughter ratios had eased through the second half of 2025, optimism around improved seasonal conditions was building, and there was growing discussion that the long-running liquidation phase may finally be ending.

However, the first quarter of 2026 has delivered a reminder that herd rebuilding in the US rarely follows a straight line.

The latest female slaughter ratio (FSR) data suggests the industry has again drifted away from rebuild territory, even as historically tight cattle numbers continue to underpin extraordinarily strong cattle prices. At the same time, worsening drought conditions across large parts of the United States are once again clouding the outlook for any rapid expansion in cow numbers.

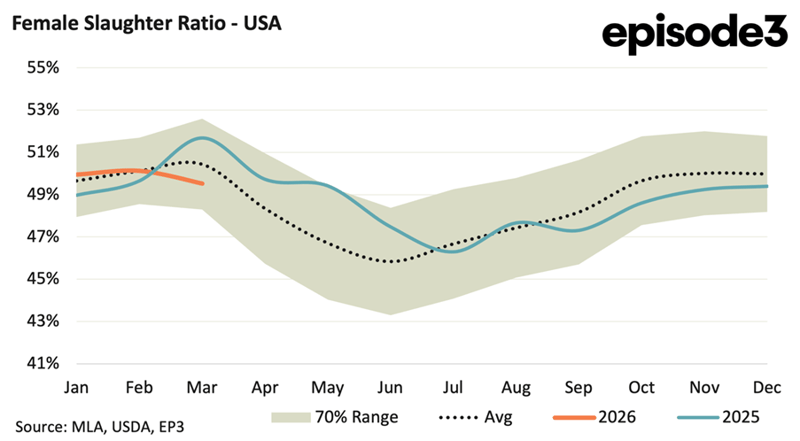

The US industry generally requires an annual female slaughter ratio below roughly 48pc to indicate genuine herd rebuilding. Above that level, the sector is typically still either liquidating or, at best, treading water.

By the end of 2025, the annual average FSR had improved to 48.8pc. That was a substantial shift from the elevated liquidation levels seen through the drought-heavy years of 2022 and 2023 and suggested the market was moving closer towards rebuild conditions.

Yet the opening quarter of 2026 has not continued that trend.

January recorded an FSR near 50pc before easing modestly through February and March to around 49.5pc. The quarterly average sits at approximately 49.9pc, notably above the rebuild threshold and much closer to historical liquidation territory.

Importantly, this does not necessarily mean the US herd is set for another major contraction phase. What it does indicate is that producers remain hesitant to aggressively retain females despite record-high cattle prices and historically tight supply.

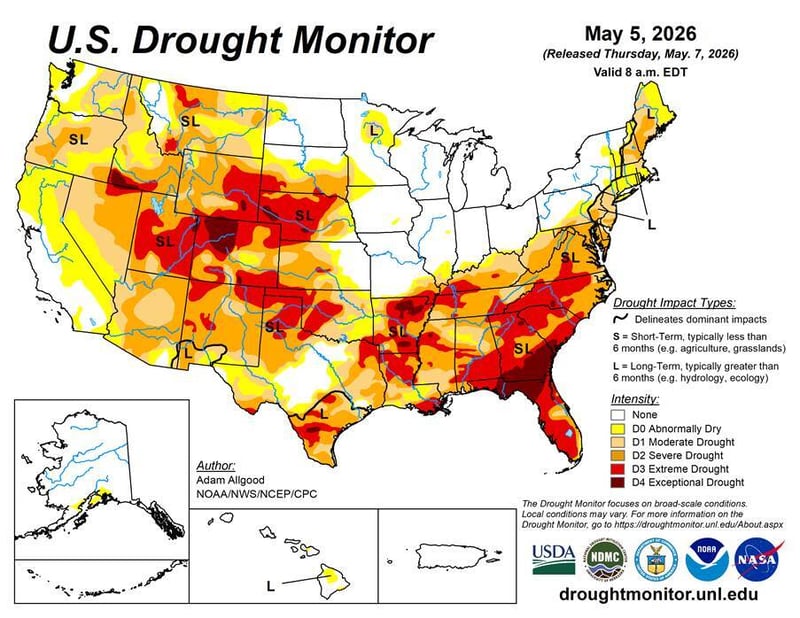

That hesitation increasingly appears tied to weather risk.

The latest US Drought Monitor highlights extensive drought coverage stretching across key cattle producing regions, particularly through the southern Plains, parts of Texas, the Southeast and sections of the western US. Large areas are sitting in severe to exceptional drought categories, with some regions experiencing both short and long-term moisture deficits simultaneously.

For cow-calf producers, drought changes the economics quickly. Even when cattle prices are attractive, deteriorating pasture conditions force difficult decisions around stocking rates, supplemental feeding costs and water availability. Retaining heifers becomes substantially harder when grass availability is uncertain and feed costs remain elevated.

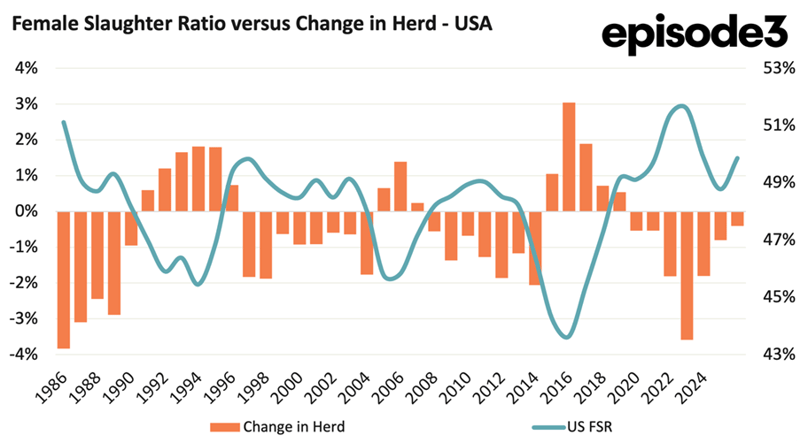

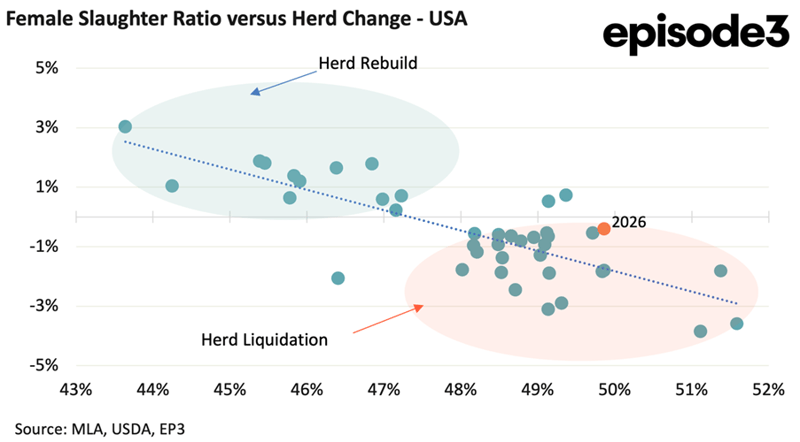

This relationship between drought and female slaughter behaviour has repeatedly appeared through US cattle cycles over the past four decades. Historically, periods where the FSR pushes above 49pc have often aligned with herd contraction phases, while sustained moves below 48pc have coincided with rebuild periods.

The current situation looks particularly interesting because the market is effectively sitting between those two zones.

Unlike the aggressive liquidation seen during some previous drought cycles, current FSR levels are not signalling panic selling. Equally though, they are not yet showing the sort of aggressive female retention normally associated with a strong rebuild phase.

That middle ground arguably reflects the broader uncertainty facing US producers.

The economic incentive to rebuild remains powerful. US cattle inventories are sitting near multi-decade lows, beef prices remain historically high, and processor margins continue to be squeezed by limited cattle availability. Tight supply conditions alone would ordinarily encourage stronger herd expansion.

However, rebuilding a herd is expensive, slow and weather dependent. A producer retaining females today is making a multi-year investment decision. If drought conditions deteriorate further, the risk profile of that decision changes rapidly. Anecdotal reporting through late 2025 and into 2026 repeatedly highlighted how renewed drought conditions across US grazing regions were delaying herd rebuilding intentions and keeping producers cautious.

The delayed rebuild also continues to have major implications for Australian cattle markets. US cattle prices remain historically elevated, with Australian cattle values currently sitting around 46pc below comparable US prices. That large pricing gap is helping maintain the competitiveness of Australian beef exports into global markets, particularly into the US itself, where imported lean beef demand remains exceptionally strong.

As long as the US rebuild remains delayed, tight American cattle supplies are likely to keep US cattle prices elevated through 2026, providing an important layer of support for Australian cattle prices domestically even as local production remains relatively large.

Historically, once liquidation phases ended, rebuilds tended to gather momentum relatively quickly. The current cycle instead resembles a stop-start transition, where producers appear willing to cautiously test rebuild conditions but remain highly reactive to seasonal volatility.

That matters globally because the pace of any US herd rebuild has direct implications for beef trade flows and cattle pricing worldwide.

A delayed rebuild phase generally means tighter US beef supply persists for longer. That supports elevated US import demand and helps underpin export opportunities for countries such as Australia and Brazil. It also prolongs the period of strong global beef pricing.

Equally, when a rebuild eventually does gain momentum, it often creates another temporary tightening in beef production because more females are retained rather than processed. In other words, paradoxically, the early stages of rebuilding can tighten beef supply further before larger calf numbers eventually arrive years later.

For now, the US industry still appears stuck near the tipping point rather than firmly entering rebuild mode. The female slaughter ratio has improved markedly from peak liquidation levels, but the first quarter of 2026 suggests the industry is not yet prepared to fully commit to expansion. Looking at the US drought maps again covering large sections of cattle country, weather may continue to dictate the timing of the next true rebuild phase more than price signals alone.

Matt Dalgleish is a director of Episode3.net and co-host of the Agwatchers podcast.

AuctionsPlus has recorded its strongest sheep clearance rate in seven years, with FY26 figures showing renewed confidence in the online livestock...

Australian beef currently remains exempt from Trump’s latest US tariff announcement, with the tariff free agreement confirmed late last year...

Every story we publish, every market wrap and weather update, is written with one audience in mind: you.